Introduction: geo manufacturing and supply chain attack and defense

Geo manufacturing is a kind of regional alliance competitiveness mixed with non economic factors. It is particularly common in the past two years. Developed industrial countries such as the United States, Japan and the European Union are emphasizing how to move the supply chain to their own countries and strengthen local manufacturing. When national security is placed above the free mobility of the supply chain and exceeds the economy, geo manufacturing begins to appear.

Geopolitical manufacturing can also be somewhat related to geopolitics. In ancient times, when the war between the Liao state and the Northern Song Dynasty continued, Prime Minister Kou zhunli advised song Zhenzong to go north, and established the alliance of Chanyuan with empress dowager Xiao, the leader of the Liao Dynasty who could not fight in this place. Both sides have their own difficult family affairs and have a strong desire for peace. This covenant was "affordable" in Liao Dynasty and "named" in Song Dynasty. The most important problem was that the territory was shelved. The exchange of money for peace has created a new diplomatic framework between neighbouring countries. In modern times, geopolitics has become the most important form of neighbor diplomacy. Manufacturing is originally relatively neutral, while economy and rationality play an important role in lubricating the friction between countries. Now, geo manufacturing is playing a greater role in technological alliance and industrial connection around national industries and enterprises.

Geo manufacturing, first of all, is the contest of national political will. On some occasions, it has become a criticized industrial policy. But now it has become Changsha tofu. It smells and tastes delicious. In order to protect large enterprises, the German government is learning; For the semiconductor supply chain, the United States is also learning.

At the macro level, any country can no longer reasonably complain about China's government subsidies. We just laugh at each other.

Recently, after receiving huge subsidies from the Japanese government, TSMC will build a factory in Japan. This action is really unusual and breaks a variety of conventions. First of all, it only serves one company, that is, Sony, the overlord of CMOS image sensors in the world. Although Sony accounted for more than half of the share, the subsequent pursuers, South Korea SamSung and Hynix, stared up like mosquitoes, which was really annoying. But the more important trouble is that the sensor can not escape the control of the chip. This time, on the land near his door, he invested 50 billion yuan with TSMC to build a special factory to solve the problem once and for all. This is the first chip manufacturing plant established by TSMC in Japan. I didn't expect to become a private factory dedicated to chip.

The most unusual thing is that the Japanese government, like the US government, will support TSMC projects in the form of subsidies. If TSMC has a hateful pursuer like Intel in the United States, it is a pure popular star in Japan. The attitude of the Japanese government is very low. In order to attract TSMC to set up semiconductor factories in Japan, it holds two 30 minute meetings every month to discuss how to "serve" TSMC so that it can set up factories.

The Japanese government's humble attitude of "attracting investment" finally moved TSMC, which is also worried and walking on thin ice despite the beautiful spring. The $8 billion investment will be an important step for TSMC to go out, and the Japanese government will invest $4 billion. Japan has its own abacus and hopes to use this opportunity to stimulate domestic manufacturers to rebuild Japan's semiconductor supply chain and reproduce the glory of the past. There is no doubt that TSMC is now a global manufacturing star. With manufacturing capacity, it seems that it has everything. The short-term industrial impression of chip shortage has exacerbated the long-term ambition of politicians to intervene in the supply chain.

Although controversial, the Japanese government feels that it is not enough. In its eyes, Europe subsidizes 1 trillion yuan, the United States 320 billion yuan and China 600 billion yuan for semiconductors. The Japanese government still has more to go. Next, the trillion yen semiconductor fund is the goal of the Japanese manufacturing industry and the government.

Supply chain stability has risen to the country's economic security. This sense of industrial division of labor rarely appears in the parliamentary halls of developed countries. The chip war, with its own strength, established the necessity of government intervention in the market. After this battle, the traditional understanding is being swept away, whether it is the visible hand of the macro government or the traditional management concept.

At the enterprise management level, the theoretical foundation of the Japanese manufacturing method established by the practice of Toyota in Japan: zero inventory is undergoing the most dangerous shaking since its establishment in the 1990s. At that time, the lean production mode -- a machine that changes the world written by Professor womach of MIT and the Toyota model written by liker of the University of Michigan in the United States created a hymn of the superiority of Japanese manufacturing and triggered in-depth simulation in the United States and the world. The "chip shortage", the shortage of containers and the zero inventory of lean manufacturing are simply vulnerable under extraordinary time. Whoever can grab enough chips is the king in the market. Even an electronics giant like apple should be cautious about using chips and shift chips from iPads to more profitable mobile phones.

The earliest signal of this "food grab" took place at the end of 2018. Huawei, which has a keen sense of smell, scrambled for goods and bought parts everywhere. This extraordinary action can be called dunkel's retreat in the supply chain, leaving valuable time for his subsequent defense war. On May 16, 2019, the United States officially sanctioned Huawei. The time advance of preparing for war and famine goes beyond the simple economy. This is simply a supply chain offensive and defensive war. It will be a useful perspective to look at the redistribution of supply chain with the cruelty of war and the mobilization of troops.

Geo manufacturing is closely related to supply chain attack and defense. It will recombine the scientific and technological advantages of the location and the manufacturing capacity of the supply chain in order to play a greater role, and the power of capital will form a strong superposition on technology and talents. The technology alliance will form a more targeted strategic cooperation. This intertwined targeted option is far from being expressed in the traditional embargo list (such as the Wagner agreement restricting the flow of specific foreign technologies to China).

Geo manufacturing is a reluctant situation for enterprises. Entrepreneurs who are at the end of an organism's blood vessels and pursue profit maximization can be said to be victims of geo manufacturing. Globalization has been hurt to some extent, and entrepreneurs must make moves and learn to respond in a hurry.

The Japanese government plans to provide a subsidy of $4 billion to Sony, which is a groundbreaking move. TSMC has opened a new hole in Japan, just like setting up a new telescope. From this point of view, the operation of the universe full of stars has undergone a more profound change. The operation mechanism of global supply chain has been very different since then.

Geo manufacturing presents the interweaving of three different forces: national will, industrial change and entrepreneurial ambition. The source of power remains unchanged, but the force bearing surface will be very different. The global manufacturing planet with established order will take on a new shape.

How will Chinese manufacturing enterprises respond? The global manufacturing pattern can be divided into three cycles: long, medium and short. Long cycle is a national contest, medium cycle is the bending of industrial form and the reconstruction of industrial plate, while short cycle is what entrepreneurs need to do to actively meet the rule of manufacturing dominance. By clarifying the ten problems in these three cycles, we can better understand the road of high-quality sustainable development made in China.

Figure 1 ten problems of long, medium and short periods

1. Have you encountered the adverse current of globalization?

The long cycle involves three issues, namely, the international countercurrent, the domestic consumption situation and the brewing new form of global supply chain.

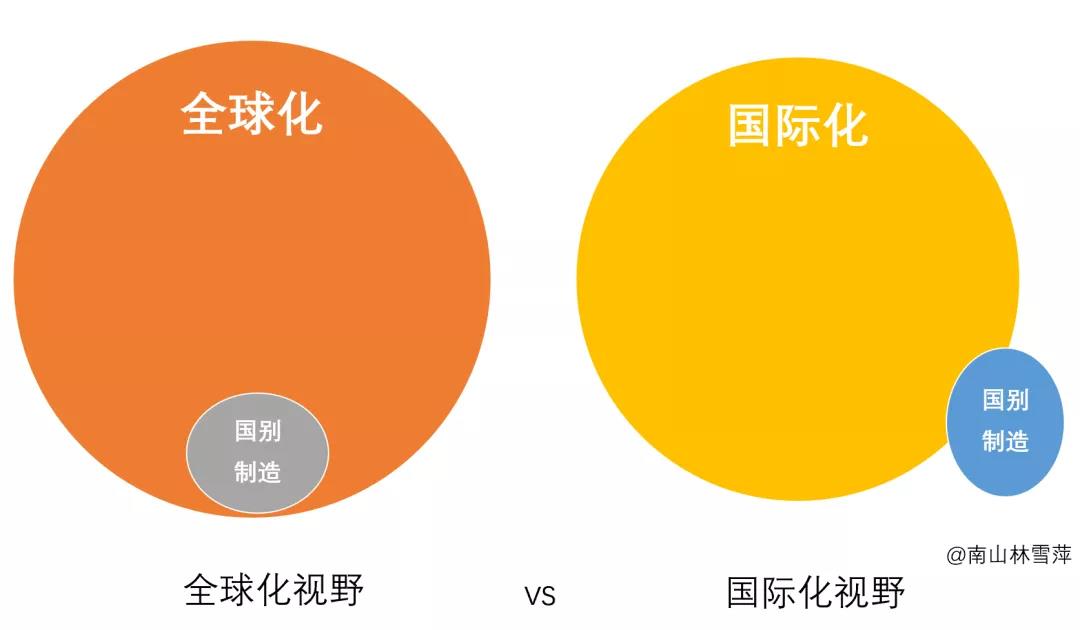

Since China's accession to the WTO in 2001, internationalization has enjoyed smooth sailing and prosperity. But there has been some resistance in the past two years. However, it is worth recognizing that this resistance is not the resistance of globalization, but only the resistance of internationalization.

Globalization is based on the relationship between subsystems and large systems, expressing "I am you"; Internationalization is the expression of "you and me" in the relationship between parallel systems. Despite geographical manufacturing, it does not deny the existence of global division of labor. Globalization is still unstoppable, but there is no doubt that the counter current of internationalization has grown a distinctive sharp corner. Every country is calculating the security and greater self-interest of its own manufacturing, which makes the difference between internationalization and globalization larger.

Figure 2 differences between globalization and internationalization

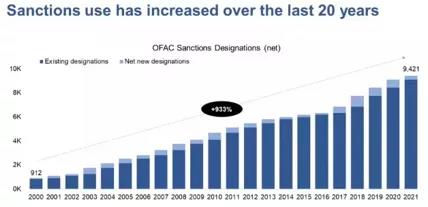

The obstruction of supply chain liquidity is the most obvious manifestation of international countercurrent. Many countries emphasize the safety of manufacturing. In fact, the flexibility and security of the supply chain has always been the most concerned issue of the U.S. Department of defense. The United States does not have such a Ministry of industry and information technology that focuses on industry, but jointly promotes it through the Ministry of defense, the Ministry of energy and the Ministry of Commerce. In the 1950s, the military industrial complex that President Eisenhower reminded the United States to be vigilant when he left office was carried forward. The development of U.S. industry is to promote civil and military dual-use, and all kinds of migrant workers' technologies have spread from military industry to aerospace. Therefore, the U.S. Department of defense is most concerned about whether the basic industrial system can effectively support the requirements of the U.S. defense industry. For more than ten years, a report on the elasticity of American manufacturing supply chain has been issued every year. In the past two years, this threat theory has become more obvious, and the actions taken are much more severe than before. This is superimposed with various sanctions imposed by the US government.

However, in October 2021, the US Treasury Department reviewed the sanctions in the past year and found that the sanctions were not particularly effective. Sanctions cases have accumulated 12000 cases (including 3000 cases that have been revoked), and the intensity has increased significantly. However, from the perspective of trade, the dependence on China has not decreased.

At the same time, the United States hopes to pull its allies together to suppress, and the allies are also skeptical.

The United States is not so effective in beating China down economically; It's not so effective to show around with carrots.

Figure 3 US Treasury sanctions assessment report 2021

Figure 4 examples of existing sanctions

Big countries wield sticks and carrots to revive manufacturing and suppress external supply chains; Small countries have only raw material resources and have limited cards to play. However, there is not much difference between the two.

Southeast Asian countries have risen rapidly in manufacturing in recent years, forming a geopolitical manufacturing that can not be ignored. Needless to say, Vietnam, like Mexico, as a neighbor of the two largest economies, fully enjoys the dividends produced by geography. Indonesia, which is rich in raw materials, is also considering how to press the lid of the pot more tightly. It is best to leave the rumbling steam in the pot. Indonesia is the world's largest exporter of palm oil (followed by Malaysia) and a large producer of high-quality nickel earth minerals essential for the development of lithium batteries. The Indonesian government is considering not exporting all raw materials - all commodities. If other countries want to use these resources for processing, they should invest in Indonesia and set up factories here. Toyota began to invest $2 billion in Indonesia two years ago to develop new energy vehicles. South Korea's LG Group has signed a battery investment agreement of tens of billions of dollars, which stipulates that at least 70% of nickel ore must be processed in Indonesia. Shangtong Wuling has already established a deep foundation in Indonesia and opened 128 distribution stores. On the territory of Southeast Asia, Japanese cars have been cultivated for many years; American brands withdrew, German brands withdrew, and Chinese cars began to kill in reverse with the advantage of electric vehicles. Geo manufacturing has made all countries think that they must hold manufacturing in their own hands. Indonesia may never think whether its industrial infrastructure can digest these raw materials. But for entrepreneurs, to enjoy Indonesia's high-quality natural raw materials and sweet sunshine, they must go deep into the Indonesian market and cooperate with the local government. Geo manufacturing, like two swords, is making a crisp impact.

If we say that mature and realistic politicians in the United States have found it impossible to fully decouple China and the United States. Therefore, the American elite are also proposing "limited decoupling" to limit the output of science and technology to a limited field. In fact, the limited sanctions method is not very established. It is easy to be like a flying dart, which may turn back and hurt yourself.

According to the documents disclosed by the U.S. Department of Commerce in late October, although they are on the U.S. supply interruption list, Huawei and SMIC still received a large number of licenses issued by the U.S. government from November 2020 to April this year, with a value of more than $100 billion. For American suppliers supplying Huawei, license licensing contracts reached US $61 billion, while SMIC received another US $42 billion. Even Huawei under the black sword, the application pass rate of American enterprises has reached nearly 70%. It's not that bad. Because if the US government starts too hard, these orders may turn to suppliers such as Japan and Europe. This is what the U.S. Department of commerce is most reluctant to see. This is also the reason why U.S. lawmakers have always wanted to promote a very specific list of disconnection, which has not been accepted by the Department of Commerce.

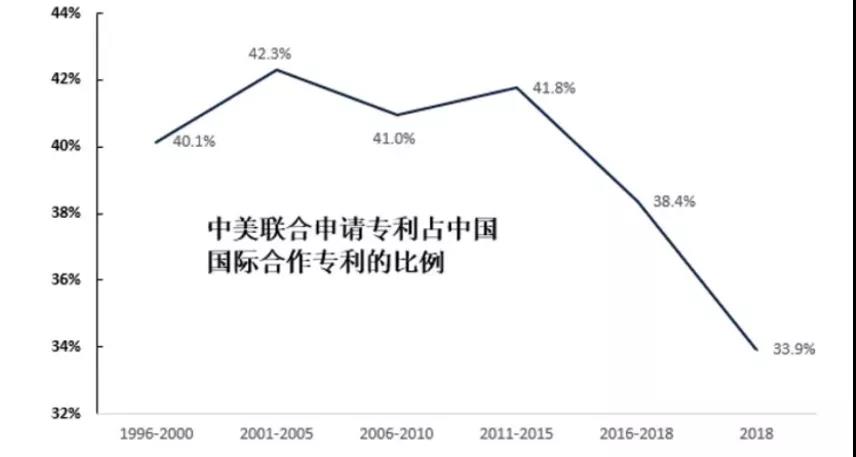

Figure 5 proportion of Sino US joint patent applications in all cooperative patents in China (source: China finance 40 people forum, Xu Qiyuan, etc.)

Not only in the trading of goods, patents are also affected. In the past two years, Sino US cooperation patents have declined sharply, but these cooperation patents have actually been digested by Japan, Germany and France. The willingness of global cooperation between world manufacturing and Chinese manufacturing still exists very strongly. If the United States seeks limited decoupling, many profits will be transferred to other countries. China may see damage, allies gain more, while the United States has a huge harvest deficit, which is what American entrepreneurs are most worried about.

2. Is high quality consumption all?

The second problem in looking back at the long cycle is the change of domestic consumption situation.

China's high-quality development can easily be misunderstood as "the growing needs of the people for a better life". But in fact, this is only a clear line of high-quality development. The most typical is to have a pressure cooker like Japan, or a kitchen utensil like German Shuangli people.

There is also a dark line, which is related to the "contradiction between the growing needs of the people for a better life and unbalanced and insufficient development". That is, high-quality consumption needs to drive the upgrading of the whole upstream supply chain at the same time. This is a situation where consumers, brand manufacturers and upstream supply chains work together.

Consumers' brand tastes are changing and have greater tolerance for domestic products. Adidas' annual report in the first half of this year shows that although it has increased all over the world, it has decreased in China. Adidas CEO lamented that the Chinese brand view has changed. By implication, Chinese people have a higher degree of convergence with domestic brands. This can be seen at many levels. The vigorous forest beverage, which has risen rapidly in the past two years, is also trying to challenge Coca Cola's youth base. At the Shanghai auto show in April, the most eye-catching booths are the convertible cars prepared by Shangtong Wuling for young people and the hard off-road vehicle tanks of Great Wall Motor Factory, while the traditional BBA vehicles are no longer the most important screen dominating role.

There is a key consumer group behind this. The consumption view of generation Z is becoming stronger. The brand view of these young people born after 1995 is very different from that of traditional consumers. People who came from the poor years after the 1960s and 1970s are more likely to have a retaliatory infatuation with foreign brands; Today's young people are more attracted to emotional communities and opinion leaders. Young people have the future.

Since consumers will not be indifferent to Chinese brands, brand manufacturers naturally can not do nothing; The more upstream supply chain should not be unimportant.

China has been planning electric vehicles since 2009, which is the first step in the world and has laid a very good first mover advantage for now. This enables the three new forces of "Wei Xiaoli" to rise rapidly. The synchronous development of power batteries has brought great development opportunities for China's equipment manufacturing. In the past, the production line equipment of the automobile factory of the joint venture company was purchased directly by foreign parties, and there was no white list opportunity for Chinese manufacturers. Now, the independent procurement of power batteries such as Ningde times and BYD has made China's laser equipment quickly kill a blood path. China's laser has experienced a golden decade of development in the past, forming a comprehensive breakthrough in the whole chain and occupying nearly 60% of the global market. Laser players all over the world must look at the Chinese market. The development of laser processing depends on the domestic industries such as power cells, photovoltaic and consumer electronics.

Starting from high-quality consumption, made in China presents a linkage breakthrough. From consumers to brand manufacturers and equipment manufacturers, we have made a breakthrough in the whole chain.

Made in China is meeting the national transportation moment, which is the crescent moon of the new production of the made in China supply chain. It needs only time to grow up.

3. Supply chain form, division of labor or vertical integration?

Then, whether there will be new changes in the form of supply chain. The answer is yes. A car, first dominated by machinery, then entered electrical control, and now enters the era of software definition. In 1995, the value of software accounted for less than 5% of the price of a car. By 2010, the proportion was 15%. By 2025, the proportion of software will reach 25%. Every step it takes forward is taken from the proportion of mechanical value. This is why both Volkswagen and BMW want to become a software company. This is not to catch up with fashion, but a struggle for profit.

From another perspective, the car has become a large mobile phone, and the OEM mode will become very common. The whole manufacturing system will undergo great changes.

The automobile manufacturing system is the most outstanding one that can affect the way of human survival.

At the beginning of last century, Mr. Ford's factory in yanzhihe was a super factory. At that time, more than 200000 people could make their own coal, chassis and even soap. The glory of 1908 seemed to belong to Ford. He made the assembly line model a symbol of the American manufacturing system. However, such a historical legend is not fair, because this year it still needs to give the other half of the era medal to Mr. Durant: this year he founded General Motors Based on Buick. Ford is a symbol of centralization. The large-scale production of a single t-car has not only created the myth of automobile, but also created a plump middle class; Durant is the pioneer of decentralization, showing diversified and distributed manufacturing. Two different production philosophies began to go their own way. Ford first gained the upper hand. When the t-car could no longer dominate, a turning point in the history of automobile development began to appear. Durant's GM quickly became the leader of the American auto industry, which is enough to prove that multi brands are more in line with different people's tastes. With the efforts of other German Volkswagen and Japanese Toyota, the global division of labor has suddenly opened up.

However, in recent years, electric vehicles have shown a new value orientation. Batteries are more like leaders. Even the most powerful apple in the world can't let Ningde era and BYD give in and build factories in the United States when manufacturing Apple cars. Volkswagen, BMW and GM will find that they need to bend down moderately to battery manufacturers. Shanghai Volkswagen has no choice but to face the "arrogant" payment terms in the Ningde era. So car manufacturers began to cooperate with battery manufacturers in different ways - if not flattery. This is especially true for chips. It is a phenomenon never seen in the hundred years of automobile history that the main engine factory shows kindness to the parts manufacturers.

Limited vertical integration began to rise.

Tesla's manufacturing method in its own factory is completely different from that of Audi and Volkswagen. Traditional automobile factories will hand over all production lines to integrators. Tesla is different. It will study the machine and buy it by itself, and then only hand over the integration of the production line to the automation integrator to do the value-added part. In other words, Tesla's understanding of machines is far better than those who built cars. Therefore, do not regard Tesla as an automobile brand company. Tesla is a genuine super manufacturing giant. In fact, Tesla's eight mergers and acquisitions in the past five years are basically all related to automation engineering. Today, its market value has easily exceeded trillion US dollars, with profound manufacturing logic behind it. A great company can shape the manufacturing system of an era.

Considering that many automobile enterprises enter parts or consider automatic driving, the pace of vertical integration is accelerating.

The most shocking industrial form in the future must come from automobiles. Here, there is no clear distinction between enemies and friends. The alliance between Ford and Volkswagen, the alliance between Honda and GM, and the joint venture between Volkswagen and Huawei will happen again and again. 360 wants to build cars and Foxconn wants to build cars, but it shows that the new form of the automobile industry is in a happy and anxious growth adolescence.

Changes driven by manufacturing patterns will reshape the pattern of the supply chain. This is very helpful for understanding the long cycle of manufacturing.

4. Made in China should give priority to the development of strategic emerging industries?

In the manufacturing cycle, the first important thing is to look at the metabolism of industrial life. For high-quality sustainable development, don't always aim at strategic emerging industries, because the foundation of made in China is still rooted in traditional manufacturing. Advanced manufacturing and traditional manufacturing are just an inverse function of time. Yesterday's traditional manufacturing is the foundation of today's advanced manufacturing, and today's advanced manufacturing is the source of tomorrow's traditional manufacturing.

Traditional manufacturing is the foundation of advanced manufacturing

Is textile a traditional manufacturing industry? Now advanced manufacturing in the United States is considering putting electronics and chips in clothes. In this way, electronic clothing can generate electricity and communicate, which is the real high technology. The high-end manufacturing innovation in the United States is to study such smart fibers on the one hand and give the manufacturing system to realize electronic clothes on the other hand.

As a manufacturing power rather than a manufacturing power, China is neither ashamed nor discouraged. China's traditional manufacturing is gradually moving towards advanced manufacturing, that is, the pyramid is built up layer by layer. It is a natural law to develop advanced manufacturing from low-end manufacturing. The water flows to the lower part, gradually accumulates, and the big water overflows the Jinshan mountain.

The reverse is different. For example, the United States is vigorously developing advanced manufacturing and wants to move all semiconductor manufacturing back to the United States. Is it really feasible? Even if the advanced processes of TSMC, Intel and Samsung are put in the United States, its back-end packaging and testing are still in Asia. This root cannot be pulled out. It is difficult for processed chips to be transported back to Asia for packaging on a large scale. For high-end manufacturing, it is very difficult to find supporting low-end manufacturing everywhere. When the water goes up, it is very cold.

High quality development is to add new wings to traditional manufacturing. In this trade war between China and the United States, China is a defensive war. There is no victory, but there is no big defeat. The US sanctions against China are now at the end of their tether.

How did China withstand the gunfire?

It does not rely on high technology, but on the fundamentals of traditional manufacturing. It is fair to say that China's high-tech manufacturing, at least for the moment, can not withstand the fire of attack and defense.

A better understanding of the improvement of traditional manufacturing is very important for understanding the transition of made in China.

Why did American auto leader aikoka become a national hero in the 1980s and 1990s? On the one hand, he created huge wealth in Ford, known as the "father of Mustang" of American economic sports car; After being accidentally dismissed by Henry Ford II, he was ordered to rejuvenate Chrysler on the verge of bankruptcy. On the other hand, his tough attitude towards Japanese manufacturing or his rescue of American traditional manufacturing is ahead of contemporary politicians and wall street.

As early as 1984, aikoka realized that basic manufacturing and high-end manufacturing complement each other. In the process of perennial competition with the Japanese auto industry, aikoka is very vigilant that Japan will empty out the basic manufacturing in the United States, because there will be no silicon valley without Detroit. Aikoka believes that high technology alone can not save the United States. It must be put together with basic manufacturing. The three major users of the computer industry (except the Ministry of Defense) are the three major automobile manufacturers: General Motors, Ford and Chrysler. If we close the door of basic industry, we will seal the silicon wafer market. Aikoka has realized that we cannot sacrifice basic industry to develop high technology, but must make the two develop together. At that time, traditional American manufacturing was being eroded by Japan. The smell of rust has just appeared, and the outspoken Italian American has smelled it. Aikoka, who has been defending industrial policy, also shouted to President Reagan and the U.S. Congress that the U.S. country needs a reasonable industrial policy, but no one listens. Today, the United States has more dangerous requirements for made in China, but the root of this dispute was initiated by made in Japan 50 years ago.

Now Chinese traditional manufacturing needs a new understanding. For example, many provinces attribute die casting manufacturing to backward production capacity. Forging and casting have always been regarded as low-end production capacity with high energy consumption and high pollution, which is easy to enter the negative list.

However, Tesla does not think so. It adopts a unique die-casting integrated process to manufacture aluminum alloy in the back of the car. It needs a 6000 ton press to achieve this. Therefore, the high tonnage die-casting machine has become a pastry in the industry. Lijin group immediately made a hundred times its fortune, and Haitian and others quickly advanced to 8000 tons. Manufacturing new technology will pull the traditional equipment to be reborn, making people unrecognizable. Therefore, it is easy to go astray to distinguish traditional manufacturing with simple cognition.

In the 819 document, SASAC talked about the responsibility and scientific and technological innovation of state-owned enterprises. The first is the industrial mother machine, and the second is the chip. This also led to the concept of industrial mother machine, which was popular with capital all of a sudden. Many people are eager to find out what the "industrial machine" is.

In fact, in addition to machine tools, industrial machine tools should also include the most conventional processes of "casting, forging, welding, heat and table". One by one, traditional manufacturing is full of high technology. Advanced manufacturing and traditional manufacturing are not separated.

5. Blindly pursuing specialization and innovation?

Made in China needs diversified attacks. We should not only pursue differences, but also be afraid of low-level tactics.

Now the whole country is praising the model of German invisible champion. Invisible champion is a development model of German small and medium-sized enterprises proposed by Simon, Germany, which seeks to be a global leader in very small fields. Specialization and innovation correspond to the invisible champion. In China, it even implicitly points to the anti card outpost of the card neck.

In fact, "specialization and novelty" can not be defined as a national hero with an emotional color. For a multi-level manufacturing country like China, specialization and innovation can only be a transitional strategy in stages. Because as long as a technology breakthrough is made, more enterprises are bound to flow in, and it is difficult to become a small number of invisible champions in the imagination. This means that the German invisible champion model may not be suitable for China. The invisible champions defined by Simon are basically global layout. Because only in the big pool of globalization can we feed the invisible champion of a country (such as Germany). If we remove the export channel of globalization and compress German manufacturing in the market of 80 million people in Germany, these invisible champions may suffocate immediately.

In China, specialized and new enterprises rarely have a global pattern. This is really a huge contradiction. Specialization and novelty means scarcity. At the other end of the tug of war, it is the most common Red Sea fleet made in China: homogeneous competition.

This is often seen as an infighting, a low-level and childish tactic, a kind of moral infighting. There was a lot of criticism.

However, the inner volume is not terrible or useless. It is the inevitable product of limited resources and limited market. The result of too many monks and too few monks is introversion. However, this is in line with the law of the market. If you can't endure the fall, you are the winner and the downstream engine. Entrepreneurship is what Drucker called the spirit of a beast. Its essence is life and death. This is the law of market competition.

Therefore, all official prices identified together will basically become invalid.

Looking at China's laser industry, with an output value of about 100 billion yuan, there are nearly 30 listed companies and more than a dozen are waiting in line. The technical context of this industry is very clear. At a glance, it is related to some companies and some people. From the result, it is a highly involute industry. But Chinese lasers are also highly evolved. Global laser sees China, and Chinese laser sees Hanshen (Wuhan and Shenzhen). Downstream equipment is very developed, such as Han Zu, lihengyuan and Deere, which dig deep trenches in the fields of PCB, power battery and photovoltaic; In the middle reaches, lasers such as Wuhan Ruike, Shenzhen Chuangxin and Shanghai Guanghui have forced IPG, an old American enterprise, to shrink back; The most upstream optical crystals such as Fujian Fujing and special optical fibers such as Changfei are also capable of fighting and fighting. The whole laser industry presents a situation of flat water, without too much short board. An internal industry does not affect the continuous evolution while fierce competition.

If we let go of the time cycle, involution is also a kind of self evolution. From an industrial perspective, the Red Sea competition is just looking for the next lower economic balance.

Specialization and innovation is the result of self optimization, and the inner volume of low-level tactics is also a mutual purification. Also worthy of respect, made in China needs diversified tolerance.

6. Can low profits be sustainable?

Made in China does show the characteristics of low profit, but this does not affect sustainable development.

Conversely, if we look at the enterprises with high gross profit, it often comes from an unbalanced industrial form. As an important industrial machine tool, machine tool needs a cam software for planning tool path. Many powerful machine tool manufacturers will develop their own, such as Beijing Jingdiao machine tool, a legend in China's machine tool industry, which has always made the machine tool shine by mastering CAM software. However, the graphics kernel algorithms of various CAM software in the world are basically monopolized by two companies, the most important one is moduleworks in Germany. In such a narrow field and large space, the company has more than 200 people, basically developers and almost no sales staff. Such enterprises can naturally enjoy 60% of the profits.

This sounds like an industry form that is too unbalanced. For larger industries, such as China's construction machinery and instrumentation industry, although there is an output value of nearly trillion yuan, the profits can not go up, because the high profits are taken away by Japanese, American or German manufacturers. There is a key generational advantage. The internal circuit boards of hydraulic machinery and instruments in Japan are basically the models of the 1980s. That was the first chip and control circuit made in mechatronics. However, as long as China does not understand, Japan and Germany can steadily eat the generation difference gross profit. The second and third generation control circuit boards have long been developed, but since China has not broken through, it is not necessary for them to adopt new technology. Kearns, the world's largest sensor, is an evergreen tree in the Japanese stock market. Its founder became Japan's richest man, surpassing UNIQLO's boss Masayoshi Yanai and son Zhengyi of Softbank. Like a local rich man, Kearns likes to hoard cash most. Cash is too abundant, but the proportion of R & D is very low, no more than 8%. What's the secret? It is to maintain the generation difference of technology, rather than pursue absolute leadership, so as to form a profit scissors gap between national manufacturing.

Therefore, it still takes time to change the current situation of low profits. Sustainable development does not exclude low profits. As long as there is profit, no matter how low, it is a prairie fire. Low profit manufacturing is the first wave of scarifiers; Higher profits may be the second wave. China is now a big country of automobile power batteries. The earliest soil is mobile phone batteries from consumer electronics. The former Scud brand carried half the sky of China's mobile phone battery. Now Scud may not be able to run, but it also has an output value of 7 billion yuan. Most importantly, it has left a large number of talents for the horizontal drift of the industry. A Scud mobile phone battery bent down and a hundred Scud car batteries raised their heads. This process is the result of knowledge flow and re flowering. Sustainable development is very likely to achieve the continuation of the industry with a baton like behavior.

7. What are the new variables for manufacturing upgrading

From the perspective of the medium cycle made in China, the most different thing from the past is that two of the three new variables are linear.

The first is the feedback of user needs. Never before have downstream users shown their meticulously nurturing thoughts towards domestic manufacturers like today. Even state-owned enterprises are carefully opening their hands to embrace domestic brand manufacturers. Only when the user factory opens the workshop site and process experience to the upstream supply chain can the upstream manufacturer make rapid progress.

The second variable is industrial capital. As long as the doorway of the industry can be made clear, capital will flock. In fact, capital is also technology blind and will blindly follow suit. After the SASAC 819 document came out, no matter what the industrial mother machine is, the stocks of the whole machine tool industry rose sharply. Like the current hot industrial software, even with an income of only tens of millions of yuan, it will be warmly pursued by investment companies. For the industrial software industry, which is used to hard life, this is really a tearful day. This also shows that any industry needs a volume so that outsiders can hear the future of the industry. As long as capital can understand, there is room for maneuver. Each industry should send the correct courtship signal, someone should speak for the industry and inject positive energy, and the industry will inject more capital.

The last variable is the spillover of basic research. Innovation comes from technology. In the end, it depends on the basic skills of quick eyes and quick hands. The focus of basic research will return to universities, colleges and research institutes. But over the years, this technology path has always been a ball of hemp, which needs a systematic repair. This is beyond manufacturing. It can be regarded as a nonlinear variable. Investing a lot of money may not work. The first two are more like linear variables, paying more and earning more.

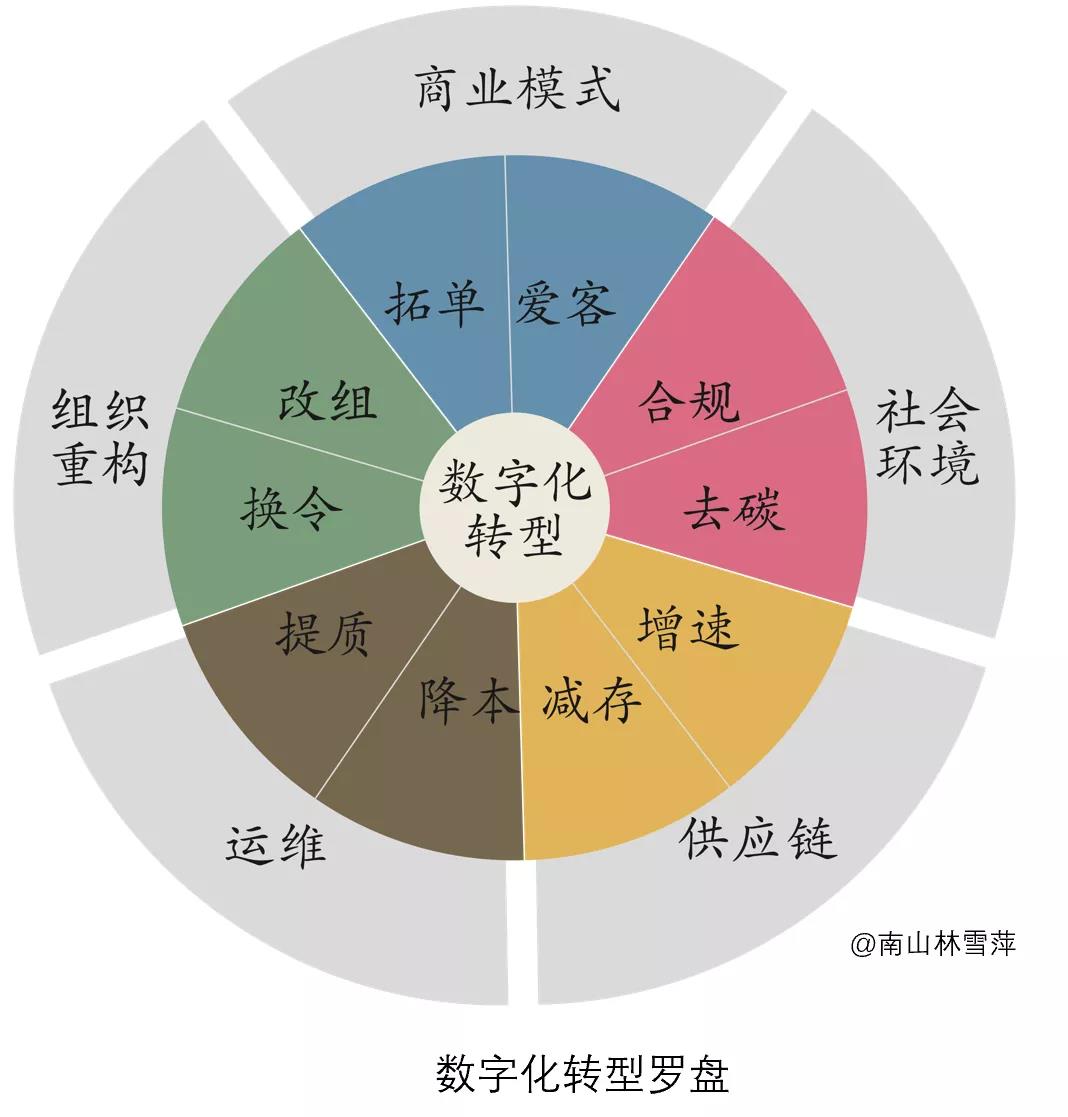

8. How to understand digital transformation

Now comes the short cycle. This is the main battlefield where entrepreneurs can make a difference. Through the long cycle, we can see the manufacturing pattern of an era. In the medium cycle, we can see the upgrading of an industry. In the short cycle, it is the entrepreneur's own stage.

Digital transformation is an unavoidable choice.

To understand the digital transformation, we can start with understanding the logic of industrial software. Mechanical products have evolved to mechatronics, and then to the current mechatronics and soft integration. The evolution logic of the whole industrial products will be easier to understand through the lens of software.

With the increasing impact of software on manufacturing, there will be a fault in the technical ability of Chinese entrepreneurs. It is not difficult to transition from a mechanical engineer to an electromechanical engineer; But from an electromechanical engineer, it is much more difficult to become a software engineer. This is a technical generation gap, which can never be handed over spontaneously. This also means that an enterprise must start from the top and supplement the software capabilities.

Marching into the software industry together is not uncommon in all fields. The top ten medical device manufacturers in the world are clearly formulating the strategy of digital transformation. Whether Medtronic, which ranks first, or Johnson & Johnson and Abbott, which follow closely, these enterprises with an income of US $100 billion are making a big and in-depth layout of remote surgery, digital nursing, etc. The core of this strategy, without exception, is achieved through the acquisition of software companies. You know, in this lucrative medical device industry, the stock capital is about US $500 billion to maintain liquidity, and the M & A of software will be a huge feast.

Figure 6 ten red flags of digital transformation

Digital transformation (see: ten red flag links of digital transformation) https://mp.weixin.qq.com/s/6T4zUj7cWxTkJ2J2rx7qcw ), you can start from multiple perspectives without sticking to one pattern (see: insert ten red flag links for digital transformation here). In terms of business model, we can start with developing orders and caring for customers; From the perspective of social environment, compliance and decarbonization must be done. As far as the dual carbon strategy is concerned, decarbonization as soon as possible has become a kind of carbon gold competitiveness.

The compass of digital transformation should always turn, move according to the times and act according to your ability. This is the ambition that needs to be established in a short cycle.

9. Is quality thinking outdated?

Quality is a commonplace problem in China, but this problem is like bean curd with too much brine, which is dead. Everyone is talking, everyone is doing things at the same pace as before.

However, with the superposition of long cycle and medium cycle, quality has become a strategic issue. If you look closely at the past, there are only four problems with all made in China: the first is that it is not built fast enough. For example, there is a market for aircraft, but now American Boeing makes 54 aircraft a month, while Chinese ARJ makes dozens of aircraft a year, which is too slow; This is still a happy thing. The second is that the manufacturing is not accurate enough. We don't know what users want at all. This is the scourge of overcapacity. Third, it is not made well enough and the quality is not up to standard; The fourth is that it is not qualified enough, such as a 14 nm lithography machine. More than 70% of these problems are related to quality. Therefore, grasping the bull nose of quality can solve most of the confusion of made in China.

Therefore, although it is an old topic, entrepreneurs should keep up their spirits, see clearly the old opponent of "quality", re-establish quality ideas and form "new quality thinking".

New quality thinking (see: new quality thinking link) https://mp.weixin.qq.com/s/diFj-Lt4rQvX6mou1of1Bg )The most important point is to add users to the quality system, and fully consider the user experience in addition to the functions. The rise of experience quality makes users no longer the farthest end outside the factory boundary, but the constraints of design and manufacturing in the factory.

Yangzhou Yangji town is the toothbrush capital of China. 80% of the toothbrushes in Chinese hotels are made here. However, when a young start-up company redesigned a toothbrush, no one in Yangji town could make it. The company had to turn to a foundry in Hebei that made high-end toothbrushes, and had to go to Japan's Toray to seek every brush wire on the toothbrush. This enterprise has redefined the quality of toothbrush, which is close to the needs of people to care for gums, so as to define a soft (no scratch) and tough (no bending) toothbrush.

This toothbrush has been a great success and has become a new favorite of people's toothbrushes.

In fact, every product around us can be redefined from the perspective of experience. We need to reinvent every wheel.

The president of Toyota American Research Institute said at the Reuters summit two days ago that not everyone needs electric vehicles. Moreover, Toyota boss Akio Toyoda has been attacking the Japanese government for being too slow in electrification. In the past three years, we can hear that Toyota has been complaining; However, in these three years, the electric vehicles of Shangtong Wuling are rapidly iterating. One of the models, Hongguang mini, has been on the market for more than a year, with a sales volume of more than 400000 units. At present, it sells more than 40000 units per month, sweeping the global ranking list. The best-selling car in China is this Hongguang mini, which has evolved into a nano customized car. In the three years Toyota complained, Shangtong Wuling has evolved six generations. Shangtong Wuling has grasped the hearts of young people in the face of user experience quality.

The national hero of the United States in the 1980s and 1990s, Chrysler President aikoka, has been emphasizing the importance of young users, including his time as Ford president. Aikoka is called "the father of Mustang" because it creates an economical sports car for young people: Mustang.

History is easy to copy and classics are easy to salute. When Shangtong Wuling puts users on the whole design and manufacturing, experience quality has become its strategic weapon to stand out.

New quality thinking is worth every entrepreneur to reset their ideas in a short time. Like computer restart, many old caches (WEB cookies) and outdated understandings need to be cleared away. The quality has been very different.

10. What kind of supply chain does the manufacturer need?

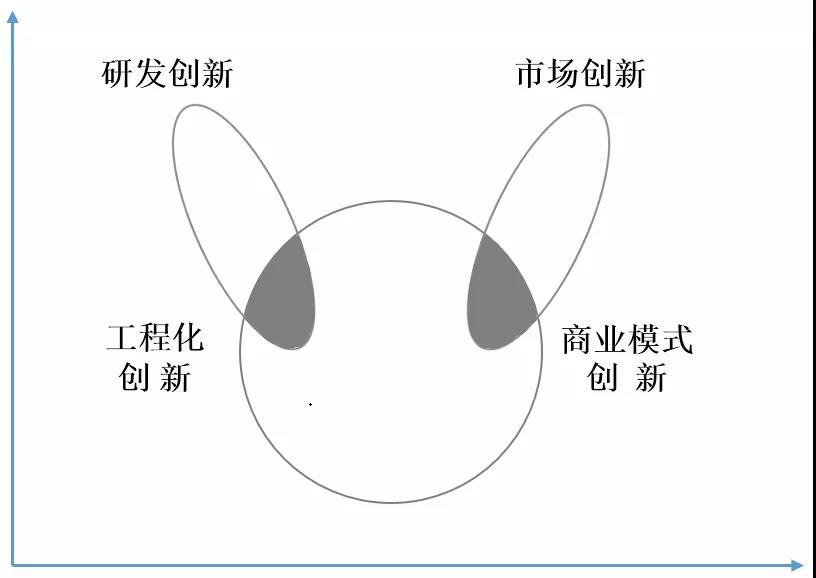

There is no doubt that made in China will now move from fighting alone to working together. However, for a long time, made in China has been trapped in the trap of smile curve. I feel that made in China is at the bottom. However, such a simple curve masks the cooperative relationship between actual partners. Made in China needs to move towards a "gray innovation". The value of the manufacturing industry is not a single line of the smile curve, but an overlapping area similar to rabbit ears. In this gray area formed by the cooperation of several organizations, knowledge flows across organizations, and innovation takes place in a mixed form. For manufacturing enterprises, not only "source innovation", "design innovation" and patents can be closely combined with upstream design and downstream users at the factory site.

Figure 7 rabbit ear curve of gray innovation

In industrialized countries, although many start-ups have good source innovation, due to the diversity and complexity of manufacturing links, they may have died on the way to start a business before they have time to accumulate enough users. The extensive and diversified soil made in China provides a lot of possibilities for incubating innovative technologies. Photovoltaic is such an example. China has become the king of photovoltaic in the world. In 2020, China accounted for 9 of the top 10 module enterprises in the world. Why did the United States invent photovoltaic technology and finally gain little in the photovoltaic industry? This should be seen from the general pattern of the international supply chain. The processing of photovoltaic industry is actually very similar to that of semiconductor. Semiconductor processing is mainly concentrated in the Asia Pacific region; Silicon materials are also mainly concentrated in East Asia. This means that the industries related to photovoltaic are basically transferred to East Asia. Germany, the United States and other countries with good development of photovoltaic industry do not have the industrial foundation for large-scale development due to the lack of supporting manufacturing technology, although they still have advantages in some subdivision technologies.

This is the manufacturing plant, which can produce a strong connection with design and users. So as to give birth to a joint innovation. This kind of joint innovation, the joint innovation between manufacturing enterprises and upstream and downstream, is in a cross zone. It is located at the junction of enterprises and presents gray characteristics.

High quality development requires rethinking the partnership of supply chain. As an entrepreneur, we need to have a better attitude of inclusiveness and cooperation and create a new type of partnership with suppliers.

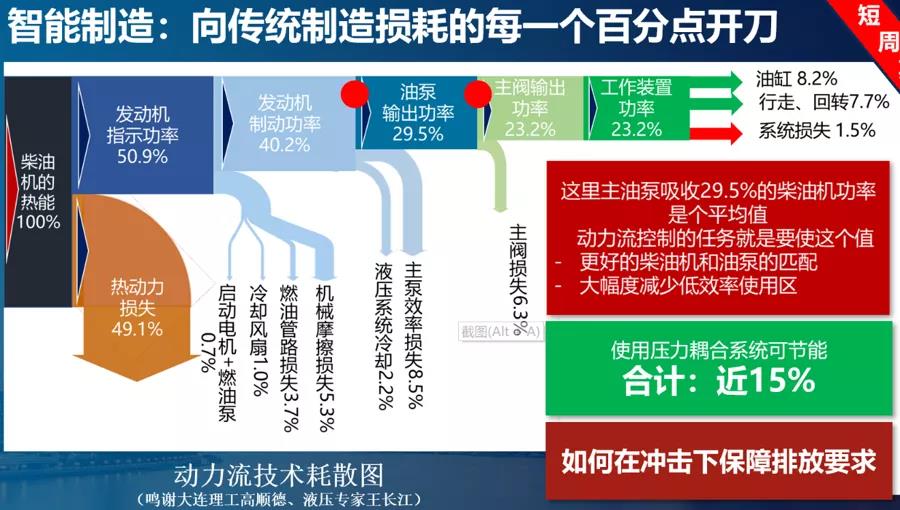

Figure 8 intelligent manufacturing should start from traditional consumption

Intelligent manufacturing is not necessarily all about intelligence and big data. We should also learn to cut every percentage point of traditional manufacturing loss. Chinese construction machinery manufacturers account for 4 of the top 15 in the world. But in fact, there are many problems. For example, there is a big gap in the efficiency of the whole machine system compared with foreign countries, and there is "air leakage" at all levels. Chinese walking machinery is still in the traditional hydraulic flow control, while foreign countries have entered the pressure control of electronic hydraulic. Control the foundation and go to a big step. Caterpillar, the world's No. 1, and hydraulic pioneer Bosch have entered the situation of electronic control, but China has not completed it yet. However, to accomplish such a thing, any enterprise, whether it is a main engine factory, a hydraulic factory or an electronic parts factory, is unable to do so. Only by combining object-oriented simulation, motion control, main engine and hydraulic plant, and even considering the advantages of 5g, can we really catch up in a group fight.

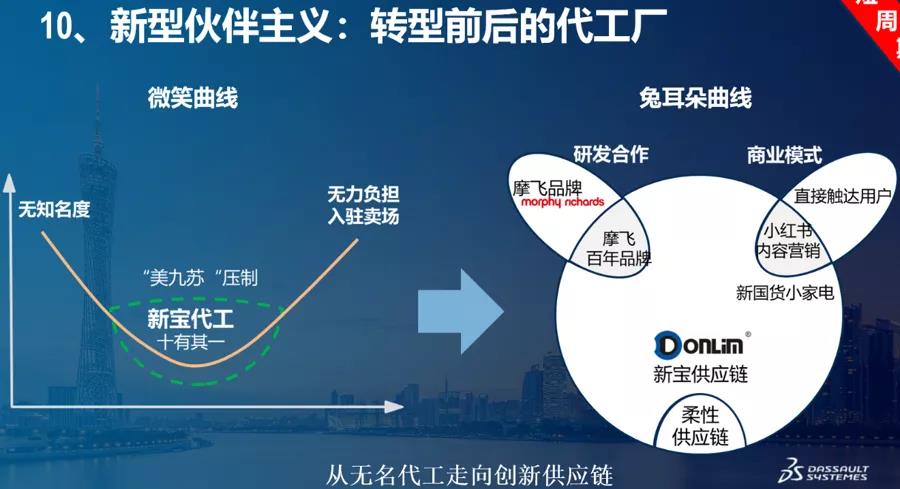

China's manufacturing capacity has precipitated a lot, but there is a way to activate it. For example, Xinbao is the OEM of many foreign small household appliance brands, accounting for nearly 10% of the export volume. However, over the years, there is no own brand. A few years ago, through the introduction of the brand and design capability of moffy in the UK, and the direct contact with users in the downstream, the flexible supply chain was re integrated. As a result, it developed very well in China. Break through the monopoly position of "Meijiu Su" (Midea, Jiuyang and SUPOR) in small household appliances for many years.

Rethinking the power of partners and building new partners with the help of the linkage ability of the supply chain is a strategy worth examining for entrepreneurs in a short cycle.

Notes: from making the most money to spending the most money

From a long-term perspective, the liquidity of the global supply chain is artificially blocked, and the supply chain offensive and defensive war begins to play a role in geo manufacturing. If it used to be driven by the economy, it is not exactly, and there is a confrontation between attack and defense. The combination form of supply chain is also showing a new situation.

From the perspective of the medium cycle, the core issue is the industry's metabolism, spitting out the old and embracing the new, the glittering color of traditional manufacturing and the diversified appearance, which is a highlight of high-quality development. Even the inevitable low profits have their own accumulation mechanism of slow growth.

From the perspective of short cycle, this is what entrepreneurs can grasp and decide most. Digital transformation, new quality thinking and joint innovation with the supply chain have become effective means to deal with the great changes in manufacturing.

Made in China is the superposition of three cycles. For entrepreneurs, from a long-term perspective, they need to look far and see the pattern; In the medium cycle, we should focus on the industry and get on the bus on time; Short cycle needs to whip yourself, re torture development thinking, and have a new understanding of digitization, new quality, partnership, etc.

In the 20 years since China joined the WTO in 2001, made in China has created a lot of foreign exchange for the country. In this sense, made in China is the most profitable industry. However, in the next 20 years, manufacturing in China will become the most expensive industry, which is close to medium and high-end manufacturing.

The moment of the National Games is ushering in a historic turning point made in China.