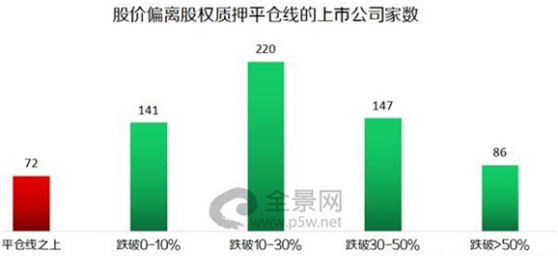

First financial analysis believes that at present, nearly 70% of the net profits of listed auto enterprises have declined. Even SAIC Group and GAC group, whose performance achieved year-on-year growth, their growth rate in the third quarter was significantly slower than that in the first half of the year. From the licensing data, in fact, the number of licensing of many manufacturers has increased negatively in March. Since June, there has been a large-scale decline in the data reported by automobile enterprises, and by September, the range and scope of the decline have further expanded.

From January to October this year, 879000 and 860000 new energy vehicles were produced and sold in China, an increase of 69.95% and 75.59% respectively over the same period last year. However, compared with the overall market scale of 29 million vehicles in China, the supply chain that can be affected is almost a drop in the bucket.Moreover, new energy vehicles, which account for only 3% of the total production and sales, are scattered in more than 200 automobile enterprises, which shows how serious the disorderly competition in the industry is.

The bubble of the Internet of things

According to the mobile Internet of things (2017) industry research report released by the research group of the school of management of Fudan University, the overall market scale of China's mobile Internet of things business will reach 1.76 trillion yuan in 2020, and the average annual compound growth rate of the market will reach 15%.

However, in practical application, limited by the technical bottleneck, many Internet of things applications are actually covered with a layer of shell, icing on the cake, and the real demand is not so strong. At present, the sales of Internet of things products (smart hardware, smart home, etc.) on the market are not optimistic, while enterprise level Internet of things projects have large investment and long cycle, and it is difficult to contribute much value for a while.

In other words, at the chip level, there are only some more sensors or communication modules. Other, the bottom layer and operating system are the back garden of giants, and there are no innovators. How many of the Internet of things industrial parks blooming all over the country have died down and how many are still surviving? How many traditional industries have been hit by the trillion scale and repeated calculation on the Internet?

Therefore, we see that there is no real giant in the field of Internet of things. Therefore, people can't wait to hype the next hot spot - AI Artificial Intelligence.

Giants such as Japan, the United States and South Korea laid off workers and fled Southeast Asia

Bern optics Huizhou factory, a giant touch panel supplier in Apple's supply chain, recently announced that it would cut 5000 dispatched workers. Flextronics, a world top 500 enterprise and well-known foundry, and its subsidiary Flextronics Plastic Technology (Shenzhen) Co., Ltd. are affected by the external environment. The company plans to arrange some employees for holidays in the following six batches from November 12, 2018 to February 1, 2019.

At the financial report meeting on November 8, 2018, Heshuo, a large apple assembly plant, disclosed that it was planning to withdraw the production line from the mainland to Taiwan or transfer it to Southeast Asia for production, so as to avoid the impact of the Sino US trade war. In addition, Taiwan factories Renbao, Weichuang, Taijun, Meilu and Kecheng, which are also Apple's supply chain, also have plans to withdraw their production lines from the mainland.

Now there is another manufacturer with such an idea. Yingyeda admitted on the 12th that the company began to prepare for the impact of the trade war a few months ago. The first wave has little impact, and the second wave is afraid to be affected. At present, it is planned that the SMT production process will stay in Shanghai. As for the later stage assembly, due to the relatively large demand for manpower, notebook computer products will be assembled in Mexico, The smart device is assembled by Penang factory in Malaysia.

Before that, Japan's Suzuki group announced its withdrawal from China, Omron and Seagate's factories in Suzhou also announced their closure, and Chuanjing motor, Daikin industry, Panasonic electric appliance and Japanese power products also moved out of China one after another.According to incomplete statistics, nearly 430 Japanese enterprises on the mainland have evacuated from China, and countless South Korean and American enterprises have evacuated.

The Nikkei research company recently surveyed 240 managers of 428 large and medium-sized non-financial companies and found that since May, only 3% of Japanese enterprises are worried about the impact of their exports in the mainland and the slowdown of mainland demand. Now as high as one-third of Japanese enterprises are worried, and another 53% of Japanese enterprises are worried about the impact of Sino US trade disputes.

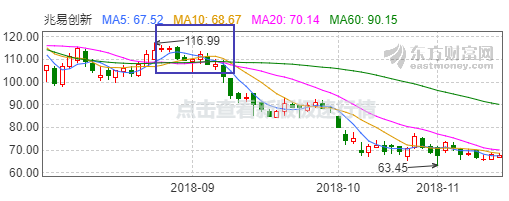

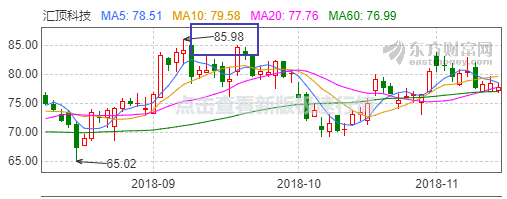

Collapsing stock market

Water overflows when it is full. In 2017, the Philadelphia Semiconductor Index rose as high as 48.62%, a record high. Chunjiang water heating duck prophet, let's take a look at the stock markets in Europe and the United States. Since October, these well-known chip stocks have gradually dropped rapidly from high levels.